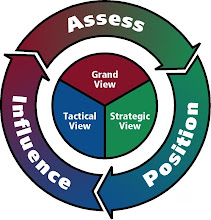

The purpose of strategic assessment is to understand the strategic valuation of one's current and future position. Regardless of the data, the emotional state can sometimes alter one's normal decision-making process.

The purpose of strategic assessment is to understand the strategic valuation of one's current and future position. Regardless of the data, the emotional state can sometimes alter one's normal decision-making process.C360 assesses the grand picture by focusing on the fundamentals, the technicalities, the various cycles and the global effect.

The front runners are those who succeed by complying with the seasonal cycle of the global marketplace . They have the strategic skill to know the entrance point and the exit point many degrees before the termination of the cycle.

"Even in the good times, you need to be conservative, totally focused and not expand beyond your means. The good times can never last forever. Things come in cycles always." --- The Unknown Strategist

One succeeds by consciously assessing the grand picture- knowing what is currently happening and what is the next occurrence, then implementing one's Tangible Vision before the cycle is over.

If you need another view on your assessment of your grand picture, contact us at service[aatt]collaboration360[ddott].com. ...

________________________________

August 21, 2009

Rise of the Super-Rich Hits a Sobering Wall

By DAVID LEONHARDT and GERALDINE FABRIKANT

The rich have been getting richer for so long that the trend has come to seem almost permanent.

They began to pull away from everyone else in the 1970s. By 2006, income was more concentrated at the top than it had been since the late 1920s. The recent news about resurgent Wall Street pay has seemed to suggest that not even the Great Recession could reverse the rise in income inequality.

But economists say — and data is beginning to show — that a significant change may in fact be under way. The rich, as a group, are no longer getting richer. Over the last two years, they have become poorer. And many may not return to their old levels of wealth and income anytime soon.

For every investment banker whose pay has recovered to its prerecession levels, there are several who have lost their jobs — as well as many wealthy investors who have lost millions. As a result, economists and other analysts say, a 30-year period in which the super-rich became both wealthier and more numerous may now be ending.

The relative struggles of the rich may elicit little sympathy from less well-off families who are dealing with the effects of the worst recession in a generation. But the change does raise several broader economic questions. Among them is whether harder times for the rich will ultimately benefit the middle class and the poor, given that the huge recent increase in top incomes coincided with slow income growth for almost every other group. In blunter terms, the question is whether the better metaphor for the economy is a rising tide that can lift all boats — or a zero-sum game.

Just how much poorer the rich will become remains unclear. It will be determined by, among other things, whether the stock market continues its recent rally and what new laws Congress passes in the wake of the financial crisis. At the very least, though, the rich seem unlikely to return to the trajectory they were on.

Last year, the number of Americans with a net worth of at least $30 million dropped 24 percent, according to CapGemini and Merrill Lynch Wealth Management. Monthly income from stock dividends, which is concentrated among the affluent, has fallen more than 20 percent since last summer, the biggest such decline since the government began keeping records in 1959.

Bill Gates, Warren E. Buffett, the heirs to the Wal-Mart Stores fortune and the founders of Google each lost billions last year, according to Forbes magazine. In one stark example, John McAfee, an entrepreneur who founded the antivirus software company that bears his name, is now worth about $4 million, from a peak of more than $100 million. Mr. McAfee will soon auction off his last big property because he needs cash to pay his bills after having been caught off guard by the simultaneous crash in real estate and stocks.

“I had no clue,” he said, “that there would be this tandem collapse.”

Some of the clearest signs of the reversal of fortunes can be found in data on spending by the wealthy. An index that tracks the price of art, the Mei Moses index, has dropped 32 percent in the last six months. The New York Yankees failed to sell many of the most expensive tickets in their new stadium and had to drop the price. In one ZIP code in Vail, Colo., only five homes sold for more than $2 million in the first half of this year, down from 34 in the first half of 2007, according to MDA Dataquick. In Bronxville, an affluent New York suburb, the decline was to two, from 17, according to Coldwell Banker Residential Brokerage.

“We had a period of roughly 50 years, from 1929 to 1979, when the income distribution tended to flatten,” said Neal Soss, the chief economist at Credit Suisse. “Since the early ’80s, incomes have tended to get less equal. And I think we’ve entered a phase now where society will move to a more equal distribution.”

No More ’50s and ’60s

Few economists expect the country to return to the relatively flat income distribution of the 1950s and 1960s. Indeed, they say that inequality is likely to remain significantly greater than it was for most of the 20th century. The Obama administration has not proposed completely rewriting the rules for Wall Street or raising the top income-tax rate to anywhere near 70 percent, its level as recently as 1980. Market forces that have increased inequality, like globalization, are also not going away.

But economists say that the rich will probably not recover their losses immediately, as they did in the wake of the dot-com crash earlier this decade. That quick recovery came courtesy of a new bubble in stocks, which in 2007 were more expensive by some measures than they had been at any other point save the bull markets of the 1920s or 1990s. This time, analysts say, Wall Street seems unlikely to return soon to the extreme levels of borrowing that made such a bubble possible.

Any major shift in the financial status of the rich could have big implications. A drop in their income and wealth would complicate life for elite universities, museums and other institutions that received lavish donations in recent decades. Governments — federal and state — could struggle, too, because they rely heavily on the taxes paid by the affluent.

Perhaps the broadest question is what a hit to the wealthy would mean for the middle class and the poor. The best-known data on the rich comes from an analysis of Internal Revenue Service returns by Thomas Piketty and Emmanuel Saez, two economists. Their work shows that in the late 1970s, the cutoff to qualify for the highest-earning one ten-thousandth of households was roughly $2 million, in inflation-adjusted, pretax terms. By 2007, it had jumped to $11.5 million.

The gains for the merely affluent were also big, if not quite huge. The cutoff to be in the top 1 percent doubled since the late 1970s, to roughly $400,000.

By contrast, pay at the median — which was about $50,000 in 2007 — rose less than 20 percent, Census data shows. Near the bottom of the income distribution, the increase was about 12 percent.

Some economists say they believe that the contrasting trends are unrelated. If anything, these economists say, any problems the wealthy have will trickle down, in the form of less charitable giving and less consumer spending. Over the last century, the worst years for the rich were the early 1930s, the heart of the Great Depression.

Other economists say the recent explosion of incomes at the top did hurt everyone else, by concentrating economic and political power among a relatively small group.

“I think incredibly high incomes can have a pernicious effect on the polity and the economy,” said Lawrence Katz, a Harvard economist. Much of the growth of high-end incomes stemmed from market forces, like technological innovation, Mr. Katz said. But a significant amount also stemmed from the wealthy’s newfound ability to win favorable government contracts, low tax rates and weak financial regulation, he added.

The I.R.S. has not yet released its data for 2008 or 2009. But Mr. Saez, a professor at the University of California, Berkeley, said he believed that the rich had become poorer. Asked to speculate where the cutoff for the top one ten-thousandth of households was now, he said from $6 million to $8 million.

For the number to return to $11 million quickly, he said, would probably require a large financial bubble.

Making More Money

The United States economy experienced two such bubbles in recent years — one in stocks, the other in real estate — and both helped the rich become richer. Mr. McAfee, whose tattoos and tinted hair suggest an independent streak, is an extreme but telling example. For two decades, at almost every step of his career, he figured out a way to make more money.

In the late 1980s, he founded McAfee Associates, the antivirus software company. It gave away its software, unlike its rivals, but charged fees to those who wanted any kind of technical support. That decision helped make it a huge success. The company went public in 1992, in the early years of one of biggest stock market booms in history. But Mr. McAfee is, by his own description, an atypical businessman — easily bored and given to serial obsessions. As a young man, he traveled through Mexico, India and Nepal and, more recently, he wrote a book called, “Into the Heart of Truth: The Spirit of Relational Yoga.” Two years after McAfee Associates went public, he was bored again. So he sold his remaining stake, bringing his gains to about $100 million. In the coming years, he started new projects and made more investments. Almost inevitably, they paid off.

“History told me that you just keep working, and it is easy to make more money,” he said, sitting in the kitchen of his adobe-style house in the southwest corner of New Mexico. With low tax rates, he added, the rich could keep much of what they made.

One of the starkest patterns in the data on inequality is the extent to which the incomes of the very rich are tied to the stock market. They have risen most rapidly during the biggest bull markets: in the 1920s and the 20 years starting in 1987.

“We are coming from an abnormal period where a tremendous amount of wealth was created largely by selling assets back and forth,” said Mohamed A. El-Erian, chief executive of Pimco, one of the country’s largest bond traders, and the former manager of Harvard’s endowment.

/// Almost everyone knows the general strategic rules. However, a few knows the exception to those rules. Do you?

Some of this wealth was based on real economic gains, like those from the computer revolution. But much of it was not, Mr. El-Erian said. “You had wealth creation that could not be tied to the underlying economy,” he added, “and the benefits were very skewed: they went to the assets of the rich. It was financial engineering.”

But if the rich have done well in bubbles, they have taken enormous hits to their wealth during busts. A recent study by two Northwestern University economists found that the incomes of the affluent tend to fall more, in percentage terms, in recessions than the incomes of the middle class. The incomes of the very affluent — the top one ten-thousandth — fall the most.

Over the last several years, Mr. McAfee began to put a large chunk of his fortune into real estate, often in remote locations. He bought the house in New Mexico as a playground for himself and fellow aerotrekkers, people who fly unlicensed, open-cockpit planes. On a 157-acre spread, he built a general store, a 35-seat movie theater and a cafe, and he bought vintage cars for his visitors to use.

He continued to invest in financial markets, sometimes borrowing money to increase the potential returns. He typically chose his investments based on suggestions from his financial advisers. One of their recommendations was to put millions of dollars into bonds tied to Lehman Brothers.

For a while, Mr. McAfee’s good run, like that of many of the American wealthy, seemed to continue. In the wake of the dot-com crash, stocks started rising again, while house prices just continued to rise. Outside’s Go magazine and National Geographic Adventure ran articles on his New Mexico property, leading to him to believe that “this was the hottest property on the planet,” he said.

But then things began to change.

In 2007, Mr. McAfee sold a 10,000-square-foot home in Colorado with a view of Pike’s Peak. He had spent $25 million to buy the property and build the house. He received $5.7 million for it. When Lehman collapsed last fall, its bonds became virtually worthless. Mr. McAfee’s stock investments cost him millions more.

One day, he realized, as he said, “Whoa, my cash is gone.”

His remaining net worth of about $4 million makes him vastly wealthier than most Americans, of course. But he has nonetheless found himself needing cash and desperately trying to reduce his monthly expenses.

He has sold a 10-passenger Cessna jet and now flies coach. This week his oceanfront estate in Hawaii sold for $1.5 million, with only a handful of bidders at the auction. He plans to spend much of his time in Belize, in part because of more favorable taxes there.

Next week, his New Mexico property will be the subject of a no-floor auction, meaning that Mr. McAfee has promised to accept the top bid, no matter how low it is.

“I am trying to face up to the reality here that the auction may bring next to nothing,” he said.

In the past, when his stock investments did poorly, he sold real estate and replenished his cash. This time, that has not been an option.

Stock Market Mystery

The possibility that the stock market will quickly recover from its collapse, as it did earlier this decade, is perhaps the biggest uncertainty about the financial condition of the wealthy. Since March, the Standard & Poor’s 500-stock index has risen 49 percent.

Yet Wall Street still has a long way to go before reaching its previous peaks. The S.& P. 500 remains 35 percent below its 2007 high. Aggregate compensation for the financial sector fell 14 percent from 2007 to 2008, according to the Securities Industry and Financial Markets Association — far less than profits or revenue fell, but a decline nonetheless.

“The difference this time,” predicted Byron R. Wein, a former chief investment strategist at Morgan Stanley, who started working on Wall Street in 1965, “is that the high-water mark that people reached in 2007 is not going to be exceeded for a very long time.”

Without a financial bubble, there will simply be less money available for Wall Street to pay itself or for corporate chief executives to pay themselves. Some companies — like Goldman Sachs and JPMorgan Chase, which face less competition now and have been helped by the government’s attempts to prop up credit markets — will still hand out enormous paychecks. Over all, though, there will be fewer such checks, analysts say. Roger Freeman, an analyst at Barclays Capital, said he thought that overall Wall Street compensation would, at most, increase moderately over the next couple of years.

Beyond the stock market, government policy may have the biggest effect on top incomes. Mr. Katz, the Harvard economist, argues that without policy changes, top incomes may indeed approach their old highs in the coming years. Historically, government policy, like the New Deal, has had more lasting effects on the rich than financial busts, he said.

One looming policy issue today is what steps Congress and the administration will take to re-regulate financial markets. A second issue is taxes.

In the three decades after World War II, when the incomes of the rich grew more slowly than those of the middle class, the top marginal rate ranged from 70 to 91 percent. Mr. Piketty, one of the economists who analyzed the I.R.S. data, argues that these high rates did not affect merely post-tax income. They also helped hold down the pretax incomes of the wealthy, he says, by giving them less incentive to make many millions of dollars.

Since 1980, tax rates on the affluent have fallen more than rates on any other group; this year, the top marginal rate is 35 percent. President Obama has proposed raising it to 39 percent and has said he would consider a surtax on families making more than $1 million a year, which could push the top rate above 40 percent.

What any policy changes will mean for the nonwealthy remains unclear. There have certainly been periods when the rich, the middle class and the poor all have done well (like the late 1990s), as well as periods when all have done poorly (like the last year). For much of the 1950s, ’60s and ’70s, both the middle class and the wealthy received raises that outpaced inflation.

Yet there is also a reason to think that the incomes of the wealthy could potentially have a bigger impact on others than in the past: as a share of the economy, they are vastly larger than they once were.

In 2007, the top one ten-thousandth of households took home 6 percent of the nation’s income, up from 0.9 percent in 1977. It was the highest such level since at least 1913, the first year for which the I.R.S. has data.

The top 1 percent of earners took home 23.5 percent of income, up from 9 percent three decades earlier.

http://www.nytimes.com/2009/08/21/business/economy/21inequality.html

1 comment:

Hey Everybody,

Below are the most recommended Bitcoin exchanges (Bitcoin for Currency):

Coinbase: $1 minimum trade

CoinMama

Get free Bitcoins with the best Bitcoin faucet rotator:

IACBit.org Faucet Rotator

Post a Comment