Does the ends justify the means?

When one is strategically positioned ahead of the competition, he can be positively optimistic. ... In an extreme competitive situation, having more positive capital than the competition is a factor.

When one is strategically positioned ahead of the competition, he can be positively optimistic. ... In an extreme competitive situation, having more positive capital than the competition is a factor.

Being ahead means the leader can make the contenders to grind purposelessly. He knows the obstacles that can be fatal and the necessary resources that are needed to stay on course.

+%28XL%29.jpg) How does one overtake the leader?"If you're last, then use yin tactics, if you are first, then use yang tactics. When you have exhausted the enemy's yang measures, then expand yin to the full and seize them. ... This is then the subtle mysterious of yin and yang according to the strategists. - Questions and Replies, 2 (from Seven Military Classics of Ancient China

How does one overtake the leader?"If you're last, then use yin tactics, if you are first, then use yang tactics. When you have exhausted the enemy's yang measures, then expand yin to the full and seize them. ... This is then the subtle mysterious of yin and yang according to the strategists. - Questions and Replies, 2 (from Seven Military Classics of Ancient China)

#

January 29, 2009Chinese Premier Injects Note of Optimism at DavosBy CARTER DOUGHERTYDAVOS, Switzerland At this year’s annual meeting of the World Economic Forum, the word optimist comes across as an ironic joke, with precious few attendees prepared to guess what comes next.Gloom is the order of the day.We cannot underestimate the challenges and dangers that the world economy faces in 2009, Stephen Roach, chairman of Morgan Stanley Asia, said at the forum’s traditional opening debate on the macroeconomic outlook. It will most likely be the first year since World War II when G.D.P. actually contracts.The only bright spot, as the conference got under way came from Wen Jiabao, the Chinese premier. Eager to calm concerns that his country’s economy would not avoid recession, Mr. Wen struck an unabashedly upbeat tone.I can give you a definitive answer, he said. Yes, it will; we are full of confidence.Mr. Wen, in a rare appearance by a top Chinese official at Davos, said that the Chinese government had set a goal of 8 percent growth in 2009, which he called an attainable target through hard work. He reeled off statistics that showed bank lending and investment, after slowing sharply in the fall, picked up in December and January.The harsh winter will be gone and spring is around the corner, Mr. Wen said.Still, the International Monetary Fund, in its new forecasts, sketched the outlines of a very tough winter indeed, economically speaking.Global economic growth will reach 0.5 percent this year, the weakest pace since World War II, the monetary fund said. That is down from a 2.2 percent prediction in November.The monetary fund also predicted that losses linked to bad mortgage loans in the United States could reach $2.2 trillion, weighing down banks worldwide. That far higher than the $1.4 trillion it anticipated in a November report.Unless stronger financial strains and uncertainties are forcefully addressed, the pernicious feedback loop between real activity and financial markets will intensify, leading to even more toxic effects on global growth, the monetary fund said.The picture in individual areas of the world was equally grim, in the monetary fund view. It foresees a 1.6 percent contraction of gross domestic product in the United States this year, and 2.6 percent in Japan. The 16-nation euro area will shrink 2 percent, it said.Despite the ambitious goal, Mr. Wen left no doubt that the Chinese were feeling the ill effects of the financial-turned-economic crisis in earnest.We are facing severe challenges, including notably shrinking external demand, overcapacity in some sectors, difficult business conditions for enterprises, rising unemployment in urban areas and greater downward pressure on economic growth, Mr. Wen said.For now, though, governments are trying to hold things together with bank bailout schemes and stimulus packages in major economies that dwarf what has ever been tried.Mr. Wen touted Chinese 4 trillion yuan stimulus package, equal to about 16 percent of gross domestic product over two years, as a large contribution to domestic demand after years of being the workshop of the world. The plan includes housing projects, rural development, railways and infrastructure, environmental protection, and recovery from last year’s devastating earthquakes.He said that feasibility studies and other institutional arrangements ensured China would be able to put the plan in place effectively.One theme that emerged early, in Davos this year, though, was that the globalization that brought national economies together in times of brisk growth demands that countries hammer out policies together on the downside. Otherwise, new government spending flows across borders, diluting its effects.We need to have coordinated fiscal response stimulus, said Justin Yifu Lin, senior vice president and chief economist at the World Bank. They are largely not coordinated.Mr. Wen largely agreed. Only with closer cooperation and mutual help can we overcome the crisis, he said.Trevor Manuel, South Africa’s finance minister, cautioned that some fiscal plans may come to nought until countries figure out how to spend money sensibly.We see a lemming-like approach: trying to get to the precipice first without having any idea what that money will do, Mr. Manuel said.I think we will have wealthy states indebted without much to show for it.And complaints about how national banking rescue plans are working also emerged.We feel that governments are encouraging banks to invest only in domestic assets, the chairman of the Dogus Group in Turkey, Ferit Sehank, said. As an advocate of globalization, I see this as a new way of protectionism.Echoing a widely held view in the global business community, Heizo Takenaka, director of the Global Security Research Institute in Keio, Japan, said fear of the future had taken over as the main driver of the crisis.The current situation is something more than a financial and economic crisis, Mr. Takenaka said. We face a confidence crisis. Once the confidence of crisis occurs, we need a strong government and central banks.The panickiest of the lot, Mr. Roach said, are American consumers, who are retrenching after a decade-long binge fed by inflated housing prices, and creating ripple effects maybe they are more like tsunamis across the world. Mr. Roach predicted that American consumers are only 20 percent into a multi-year adjustment that will leave them much more frugal.Chinese exports have already declined quarter-on-quarter, he said.Shipments from Taiwan and Japan are also down. As the Chinese economy has hit a wall, the rest of Asia has followed suit, Mr. Roach said.Mr. Manuel, of South Africa, said the economic crisis has hit his continent hard in the past year, as projects to develop natural resources, an area with much potential for Africa, are scaled back.In the Democratic Republic of Congo alone, 48 mining projects are in various stages of abandonment, Mr. Manuel said.Look at Africa, he said. It’s a risk of decoupling, derailment, and abandonment altogether.Mr. Manuel and others said that as Western and Asian governments start borrowing heavily to spend for stimulus packages, they should allocate a portion to poorer countries.Copyright 2009 The New York Times Companyhttp://www.nytimes.com/2009/01/29/business/29econ.html

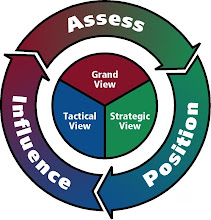

To properly compete in the global economy, the successful strategist and his/her project team usually know what are their objectives. They assess their grand settings in order to determine what are their possibility of success. The assessment also acts as a compass for the strategist (and the team) to decide what circumstances work for them. The next step is the development of a grand strategic overview that is consisted of a goal, a set of strategic guidelines based on our PACE format, a listing of PACE-specific objectives.

To properly compete in the global economy, the successful strategist and his/her project team usually know what are their objectives. They assess their grand settings in order to determine what are their possibility of success. The assessment also acts as a compass for the strategist (and the team) to decide what circumstances work for them. The next step is the development of a grand strategic overview that is consisted of a goal, a set of strategic guidelines based on our PACE format, a listing of PACE-specific objectives.

+%28XL%29.jpg)