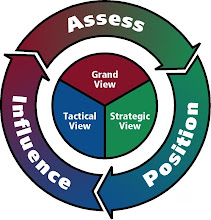

Start by understanding the grand settings by reading Chapter 1 and Chapter 13 of Sun Zi's Art of War (Sawyer or Ames translation).

Then, read Sawyer's translation of 100 Unorthodox Strategies in understanding how to create strategic influence by playing the "pre-positioning to compete" game.

It is important to understand the culture, the history and the mindset behind the game before playing the game.

###

China's Market: Vital but Tricky

By MATTHEW MONKS

August 22, 2007; Page B3A

Baird Capital Partners got a lesson in China's cutthroat business culture a couple of years ago when a plastic-molding company it owned tried to set up a joint venture there.

While reading the fine print of an agreement between Xaloy Inc. and a local manufacturer, Baird Capital came across a passage indicating that the Chinese entity planned to set up a sister company with access to Xaloy's proprietary technology.

Baird, a unit of Robert W. Baird & Co., realized the joint venture was a ruse when it slipped a noncompetition clause into the agreement, and the other party pulled out of the deal. According to Baird, the local company essentially wanted to crib Xaloy's intellectual property and set up its own operation. Baird says it might not have picked up on the ploy if it hadn't had a team of investment professionals embedded in the country.

"You can't manage Asia from afar -- the laws are evolving, the culture is evolving," said Andrew Brickman, a partner with the Milwaukee firm. "The most viciously competitive market in the world is Asia."

/// *** To play the China game, it is important to establish a base camp. One objective of establishing A part of the base camp is quietly pre-positioning a team of high-qualified competitive intelligence professionals to understand the grand settings of your marketplace. The success of this particular step enables the team to establish the stage of advanced base camp.

It is also one of the most complicated markets, but Asia is increasingly an essential ingredient of doing business for many midmarket companies. That combination is prompting more U.S. midmarket buyout firms to open offices in China to help shepherd their portfolio companies through the tricky process of sourcing goods and establishing manufacturing sites in the region.

While megafund managers like Carlyle Group and Blackstone Group LP have had a presence in China for years, only recently have their midmarket colleagues followed suit. At least four have opened offices in China in the past year or so: American Securities Capital Partners LLC, Sun Capital Partners Inc., Anderson Group and Hammond Kennedy Whitney & Co. They join a small number of midmarket firms that have been there for longer, including Baird and Blue Point Capital.

There is no blueprint for setting up shop, with the new entrants varying in how they pay for their new branches and how many people they commit to the effort. Some firms, like Anderson Group, charge their portfolio companies fees to support the new offices. Others, like American Securities, rely on the general partners to absorb the costs.

/// *** Step 1: To play the China game, understand what is the big picture. Having a Tangible Vision will be helpful.

These firms say that expanding overseas is no easy task, as reliable talent is hard to find and office space in cities like Hong Kong and Shanghai is expensive. Becoming global also puts stress on a firm's culture, as lengthy overseas flights and 6 a.m. conference calls become a day-to-day reality.

"It's a lot of money, and it's even more time and effort," said Michael G. Fisch, president of American Securities Capital.

/// *** Compass AE methodology enables a distant team to collaborate efficiently by focusing on the goal and objectives

But they add that midmarket investors have no choice but to pay attention to China as U.S. manufacturing shifts overseas.

For instance, Blue Point portfolio company Engineered Material Solutions Inc., which makes metal strips for the automotive and telecommunications industries, recently opened a production facility in Eastern China under pressure from customers. Automobile brake and component maker Qualitor Inc., in which Baird has a stake, had to open a site in China or else lose a contract with a top customer that recently moved production to the region.

"The middle market's customer base is heading to Asia," Mr. Brickman said. "Asia is not going anywhere. You have to deal with the global economy because ignoring it will only threaten what you're trying to do."

A presence in Asia can also give a firm a competitive edge in making deals. Blue Point structured its bid for Dri-Eaz Products Inc. last year by taking into account cost savings the dehumidifier maker could generate by sourcing parts in China.

"We bid more sharply than we would have otherwise," said Blue Point Managing Partner Chip Chaikin. "It allowed us to be a little more aggressive."

His firm also makes it a point to sell its capabilities in Asia to U.S. investment banks, and took a handful of them on a weeklong tour of the country about a year and a half ago. The visit impressed Lincoln International, which now keeps Blue Point in mind when it is advising a business that has facilities in China or is looking to source products in the region.

Having an office in China "gives them a competitive advantage in actually winning deals in the U.S." said Jim Lawson, managing director and co-chairman of the Chicago bank. "Private-equity firms are trying to distinguish themselves in some way. This Asian play is a way to distinguish yourself."

Just how firms go about that varies. For instance, Hammond Kennedy has just one director in Shanghai -- a Chinese native who had worked for the firm in the U.S. since 2004 and relocated last year. Baird Capital, in contrast, has a 20-person team spread across offices in Hong Kong, Shanghai and Beijing.

Anderson Group, which buys U.S.-based manufacturers valued at less than $100 million, has staffed its Shanghai office with a partner, a chief financial officer and two sourcing specialists with connections in the plastics and metals industries.

The team essentially acts as a chaperone for Anderson Group portfolio companies looking to source goods in the region. It handles everything from making travel arrangements for visiting business executives to helping navigate the complex legal wrangling it takes to establish a manufacturing plant.

For Anderson Group, its China office represents a major change in strategy. For most of its 27 years in business, the firm took pains to avoid investing in companies vulnerable to competition from China, considering the region a threat. That changed in 2005, when it made a play for TexStyle LLC, a U.S.-based bedding and curtain maker with facilities in Shanghai. The investment opened the firm's eyes to the advantages of sourcing goods in the region, prompting it to establish the office.

"We shouldn't be looking at China as a strategic threat," said Corey Gaffney, a partner with the firm. "It really should be an opportunity."

/// "For every crisis, there is an opportunity. ..." --- A favorite saying of amateur strategists.

/// "The key to responding to an crisis is understanding its impact and what position of the cycle is the crisis at." --- A favorite saying of Ultra Class strategists.

Source: http://online.wsj.com/article/SB118772068541604283.html

Copyright 2007 Dow Jones & Company, Inc. All Rights Reserved

###

In Asia, It's a World of Extremes

China's Insular Markets

Defy Slump in Shares;

Other Trends Pose Worry

By JAMES T. AREDDY

August 20, 2007; Page C1

SHANGHAI -- Can China's stock market remain hot amid a global chill?

The world-wide contagion of credit concerns that started with the U.S. mortgage market has driven down almost every significant global stock index this month, from São Paulo to Paris to Singapore -- except for China's Shanghai Composite Index. The Chinese benchmark slid slightly last week, mainly on domestic concerns, but remains up about 4% since the beginning of August -- and up 74% this year.

The Chinese market has been insulated from the global market chaos by strict capital controls that largely prevent international investors from buying domestic Chinese stocks -- and that tightly limit overseas investing by Chinese. So any reversal in China would have little direct impact on global capital flows. But the fall of one of the few pillars of global market strength could damage investor sentiment -- which remains shaky despite Friday's move by the Federal Reserve to cut its discount rate and encourage banks to borrow.

For now, analysts say, there is no reason the global credit crunch has to spread to China's stock market if trouble remains confined to global financial markets. China is still so swimming in cash that its central bank recently drained funds from its financial system while its global counterparts were pouring money into theirs. But the sustained rise in Chinese shares means many analysts believe it is due for a correction at some point -- even if no one can say when.

The U.S. credit problem "can't affect China directly," says Andy Xie, an independent economist in Shanghai. But, he adds, "I think the Chinese stock market is a bubble."

China's stock market is less than 20 years old, and investors, many of them new to the game, often trade on rumors or even superstition rather than fundamentals. Other unhealthy trends persist: Many companies have been buying stock and using the rise in prices to boost their earnings -- a trend that could add painfully to any downturn by hammering corporate profits, and thereby fueling more selling.

China's market still doesn't play the central role its counterparts do in more developed economies. But the market is starting to emerge as a closely watched indicator for the Chinese economy, which this year will become the world's third largest, after the U.S. and Japan. Already once this year, in February, a market swoon in China startled markets elsewhere. Mounting uncertainty about U.S. economic growth makes China's economy, and its market, more important in investor eyes.

For economists gauging the outlook for China's markets, one key question is whether weak global markets might translate to softer demand among consumers in the U.S. and elsewhere -- and thereby slow China's exports, which are a major contributor to the economy. About one-fifth of China's exports go to the U.S., leaving China's economy "potentially very vulnerable to any substantial future U.S. consumer pullback," Michael Kurtz, a Hong Kong-based strategist at Bear Stearns, said in a recent note.

Since China's bull market began in July 2005, it has risen by 3.6 times. That has brought total capitalization of its two exchanges, in Shanghai and Shenzhen, to about $2.8 trillion -- about the size of its annual gross domestic product. That isn't high compared with other countries, but it does suggest any major market setback could cause broader economic fallout than has happened in China in the past. By contrast, the country's last bear market, in the first half of this decade, had no apparent impact on broader economic growth.

Few consider Chinese stock prices cheap: Shanghai-listed shares trade at an average 55 times last year's earnings. Yet among China's retail investors, confidence remains high. In the first half of August, 1.78 million new trading accounts were opened. A week ago, as credit worries were pounding global markets, $7.8 billion was pledged in a day to the launch of a mutual fund offered by China Post & Capital Fund Management Co. Friday, three initial public offerings made their debuts in China, rising an average of more than 300%.

The Shanghai Composite Index did decline for three straight days late last week. It ended the week at 4656.57, about where it was 10 days earlier, holding a gain of 4.1% for the month. Moreover, the main cause for last week's slip came not from global credit worries, analysts and traders said, but from domestic concerns that underscore how starkly different China's current situation is from much of the rest of the world. One key factor: A surge in inflation fueled worries of another interest-rate increase.

The market also ran up against psychological resistance as it neared the 5000 level for the first time -- but few see that as insurmountable for an index that pulled above 2000 for the first time just last November.

China's market is a "rational bubble," says Walter Lin, chief representative in Beijing of Aviva PLC's Morley fund-management unit. "It is a largely closed market, and we have excess liquidity here," he says.

While Chinese investors believe they are acting sensibly by continuing to pile into the market, history is replete with examples of how traditional market fundamentals ultimately squash talk that a particular market is unique.

And while other markets have been hurt in part by big investors selling off holdings elsewhere to compensate for losses in the U.S., foreign investors have virtually no role in China. About 50 foreign institutions share a $10 billion quota to make investments in China's local-currency stock and bond markets -- meaning foreigners own a total of less than 0.5% of China's stock-market capitalization. Foreigners also can trade Class B shares, denominated in U.S. or Hong Kong dollars, but the total value of those shares is tiny, and they have almost no effect on the broader market.

Because the global credit problem "didn't change the trend of the China stock market," this small pool of foreign money managers hasn't noticeably altered strategy, according to a top official at a Shanghai brokerage who handles much of the trading.

To some degree, China's stock values have simply been catching up with broader advances by its economy: The Shanghai Composite fell 38% between the end of 1999 and 2005, while GDP more than doubled. Market capitalization plummeted to 18% of GDP. The current rally was triggered in mid-2005 by a government change to shareholding structures that gave minority investors a bigger voice.

--Zhou Yang in Beijing contributed to this article.

Write to James T. Areddy at james.areddy@wsj.com

http://online.wsj.com/article/SB118755553396602201.html

No comments:

Post a Comment