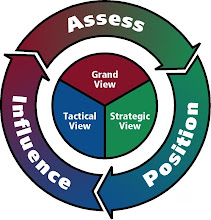

When negotiating with a trading partner, assess the competitive position of each side. Then, determine who has the advantage of time and resources. Do not rush into the situation. It is recommended to properly build a detailed plan that is based on assessed data. The greater your advantage of time and resources is, the greater your leverage becomes.

Revised content from the wiki page on the 36 Stratagems.

The View of China

Watch the fires burning across the river (traditional Chinese: 隔岸觀火; simplified Chinese: 隔岸观火; pinyin: Gé àn guān huǒ) Delay the entering of the field of battle until all the other players have become exhausted fighting amongst themselves. Then go in at full strength and pick up the pieces. Usage This "Opportunistic Stratagem" thrive on situations where vulnerabilities can be exploited. The objective is to capitalize on all opportunities so as to gain the advantage. # "Looting a house on fire" (趁火打劫 or "Chen Huo Da Jie")

When an organization is beset by internal conflicts, they are not able to deal with an outside threat. This is the time for a superior organization to make a deal that gives them leverage.

Usage

Gather internal information about the opposition. If the opposition is in its weakest state ever, conquer the opposition without mercy.

The View of Russia

Russia possesses no strategic options to gain any leverage in its dealing with China. Their initial objective is to fix their economy first.

#

[ Turning Crisis into Opportunit

(From Stratfor.com)

China and Russia struck a deal that will give Russian energy firms Transneft and Rosneft loans to increase East Siberian oil field development and production and to connect the Eastern Siberia-Pacific Ocean pipeline to China. In return, China will receive about 300,000 barrels per day of oil for the next 20 years. Russia might have made the deal out of economic desperation as its state-owned energy firms feel the pain of evaporating credit, economic woes and low oil prices.

China and Russia struck a deal that will give Russian energy firms Transneft and Rosneft loans to increase East Siberian oil field development and production and to connect the Eastern Siberia-Pacific Ocean pipeline to China. In return, China will receive about 300,000 barrels per day of oil for the next 20 years. Russia might have made the deal out of economic desperation as its state-owned energy firms feel the pain of evaporating credit, economic woes and low oil prices.

China and Russia reached an agreement under which China will give key Russian energy firms Rosneft and Transneft loans for $15 billion and $10 billion, respectively, Transneft spokesman Igor Dyomin said Feb. 17. Russian state-owned oil pipeline company Transneft will use its loan to connect the long-delayed Eastern Siberia-Pacific Ocean (ESPO) pipeline to China, and Rosneft will use its loan to expand East Siberian oil field development and production. In exchange for the loans, the Chinese will receive about 300,000 barrels per day (bpd) of oil for the next 20 years.

The loans are part of the much longer negotiations circling the idea of the ESPO pipeline. It makes perfect sense for Russia to link its vast Eastern Siberian oil resources (about 10 percent of Russia’s total oil reserves, or 10 billion barrels) to energy-consuming Asian markets like South Korea, Japan and especially China. Moreover, a pipeline that could carry Russian oil to the country’s Pacific coast could supply markets even further abroad, such as the United States. The problem is that building a pipeline across thousands of miles of mountainous Siberian terrain requires enormous capital investments that are not easy to come up with, particularly during a global recession. During Soviet times, the Russians used central government investment to undertake gigantic energy infrastructure projects (such as the pipelines from the Yamal Peninsula to Europe) that served strategic interests. After the Soviet collapse, and especially during Vladimir Putin’s presidency, Russia has been demure about such capital projects, performing only what was absolutely necessary to maintain exports to existing markets and passing up major renovations or expansions. This tight-fistedness enabled Russia to build up massive foreign exchange reserves with its trade surpluses, but it meant that many potential plans remained on the drawing board.

A new opportunity emerged when the Chinese and the Russians began negotiating the deal that has just been settled. The Chinese would loan the money, and a 44-mile spur off the ESPO pipeline would be jointly built and operated, linking Skovorodino in Russia’s Amur region to Daqing in China’s Heilongjiang province. When Transneft offered to build the spur, negotiations began. Despite hard-bargaining tactics and inherent distrust between the two geopolitical rivals, the proposal always seemed promising, since it marked such a close alignment of interests. Without Chinese capital, the Russians were unlikely to realize their strategic goal of transporting resources to new markets in the East at a time when their main market — Europe — is turning away. Without Russian oil, the Chinese would not be able to diversify their oil supply and enhance their energy security.

But the proposal ignited a conflict between the two major Russian players, Transneft and Rosneft, over the fact that a pipeline leading directly to China limits Russia to one customer, whereas building the pipeline to the Pacific coast would allow supplies to be shipped to any number of buyers. Rosneft wanted to secure China as a customer first, and then go on to bigger and better things; Transneft wanted to run a line straight for the coasts (to prevent China from taking advantage of a direct line by re-exporting Russian oil or by unilaterally demanding price reductions), or to refine the oil at home and continue shipping products by rail to the Pacific.

Rosneft is one of Moscow’s energy champions, and also has the support of one of two major political factions in the Kremlin, led by Deputy Prime Minister Igor Sechin. Ever since Rosneft assimilated the broken pieces of former Russian energy company Yukos (with help from a $6 billion loan from China in 2004), it has depended on developing its Siberian potential in order to rise above its many competitors. ESPO is therefore crucial to Rosneft’s survival and success. Therefore, Rosneft wanted to secure the deal with China first so as to have a stepping stone to a broader Far East strategy.

Negotiations on the Chinese deal were delayed. The Chinese were reluctant to sign an agreement while they had doubts about whether the Russian oil producer and pipeline builder could get along — specifically, China was waiting to see whether Rosneft would have the Kremlin’s support. Beijing also knew it had control of the purse strings; and given its inherent distrust of the Russians, it wanted to be sure that the agreement was fully to its liking — for instance, by insisting, against Putin’s demands, that the loan be made in U.S. dollars and not Russian rubles. China also wanted to make sure it did not need the cash to address any immediate problems at home due to the financial crisis.

Ultimately, the Kremlin intervened in the spat between Rosneft and Transneft, approving of Rosneft’s strategy and enabling the deal to move forward — by endorsing a slew of tax reforms and incentives for oil development and export in key East Siberian sites such as Sakha, Irkutsk, Krasnoyarsk, and eventually Taymyr, Sakhalin, Lena-Tunguska and Lake Baikal. The Chinese then came forward with the $25 billion, with a 6 percent yearly interest rate (moved down from 7 percent), which means that Russia gets the cash up front while China receives about 2.2 billion barrels of oil.

The deal reveals several things about the way regional geopolitics are unfolding as the world economy contracts. Russia and its state firms are in need of a lifesaver now that the combination of low oil prices, the absence of outside credit, and domestic financial troubles has rapidly depleted their reserves. The Chinese loan will provide an infusion of cash at just the right time to stave off financial pressures, allowing the Russians to undertake otherwise unfeasible projects that will pay off when Chinese energy demand revives. Moscow will see its Far East strategy advance another rung up the ladder, while Sechin’s clan, having scored a major victory in winning Kremlin approval for the Chinese deal, will gain an economic and political advantage over rivals.

China, meanwhile, will receive a steady stream of oil for the next 20 years. Rosneft’s facilities are ready to produce about 313,000 bpd (slightly more than the agreed-upon amount to repay the loan) at Vankor, the key Siberian site for the ESPO project. This amount of oil to be paid to China is roughly the same as the amount imported from Russia in 2007 (mostly by rail), and about half as much as the 600,000 bpd rail capacity in the region. This is significant, especially for a country so dependent on manufacturing and sensitive to energy shocks. China needs a reliable energy supply and does not want to be overly dependent on energy from one source. Moreover, most of its oil is shipped via ocean from the Middle East, and this leaves China at the mercy of U.S. naval power. However remote the possibility of an interdiction, it is enough to make a landlocked oil supply route attractive to Beijing.

But for Russia the deal is not a win-win. Moscow is getting pounded by the recession, and the decision to go forward on a pipeline that goes directly to China, forgoing the possibilities offered by a more versatile sea port destination, is a major concession. Obviously, now the Russian firms have to go through with the infrastructure developments, which will be technically demanding and fraught with unforeseen expenses and delays (sending Siberian oil eastward is said to cost twice as much per barrel as sending it westward). And the Chinese got a steal: Although not all of the contract’s subtleties are likely out in the open right now, reimbursement for the loan means that the Chinese have purchased Rosneft crude for only about $11.40 a barrel once interest is figured in — about one-third of what Russia’s crude fetches on the open market right now. The Russians have essentially locked the fate of their Far East strategy to the whims of Chinese energy policy, and this is a compromise that could reveal how financially desperate Russia is.

China and Russia reached an agreement under which China will give key Russian energy firms Rosneft and Transneft loans for $15 billion and $10 billion, respectively, Transneft spokesman Igor Dyomin said Feb. 17. Russian state-owned oil pipeline company Transneft will use its loan to connect the long-delayed Eastern Siberia-Pacific Ocean (ESPO) pipeline to China, and Rosneft will use its loan to expand East Siberian oil field development and production. In exchange for the loans, the Chinese will receive about 300,000 barrels per day (bpd) of oil for the next 20 years.

The loans are part of the much longer negotiations circling the idea of the ESPO pipeline. It makes perfect sense for Russia to link its vast Eastern Siberian oil resources (about 10 percent of Russia’s total oil reserves, or 10 billion barrels) to energy-consuming Asian markets like South Korea, Japan and especially China. Moreover, a pipeline that could carry Russian oil to the country’s Pacific coast could supply markets even further abroad, such as the United States. The problem is that building a pipeline across thousands of miles of mountainous Siberian terrain requires enormous capital investments that are not easy to come up with, particularly during a global recession. During Soviet times, the Russians used central government investment to undertake gigantic energy infrastructure projects (such as the pipelines from the Yamal Peninsula to Europe) that served strategic interests. After the Soviet collapse, and especially during Vladimir Putin’s presidency, Russia has been demure about such capital projects, performing only what was absolutely necessary to maintain exports to existing markets and passing up major renovations or expansions. This tight-fistedness enabled Russia to build up massive foreign exchange reserves with its trade surpluses, but it meant that many potential plans remained on the drawing board.

A new opportunity emerged when the Chinese and the Russians began negotiating the deal that has just been settled. The Chinese would loan the money, and a 44-mile spur off the ESPO pipeline would be jointly built and operated, linking Skovorodino in Russia’s Amur region to Daqing in China’s Heilongjiang province. When Transneft offered to build the spur, negotiations began. Despite hard-bargaining tactics and inherent distrust between the two geopolitical rivals, the proposal always seemed promising, since it marked such a close alignment of interests. Without Chinese capital, the Russians were unlikely to realize their strategic goal of transporting resources to new markets in the East at a time when their main market — Europe — is turning away. Without Russian oil, the Chinese would not be able to diversify their oil supply and enhance their energy security.

But the proposal ignited a conflict between the two major Russian players, Transneft and Rosneft, over the fact that a pipeline leading directly to China limits Russia to one customer, whereas building the pipeline to the Pacific coast would allow supplies to be shipped to any number of buyers. Rosneft wanted to secure China as a customer first, and then go on to bigger and better things; Transneft wanted to run a line straight for the coasts (to prevent China from taking advantage of a direct line by re-exporting Russian oil or by unilaterally demanding price reductions), or to refine the oil at home and continue shipping products by rail to the Pacific.

Rosneft is one of Moscow’s energy champions, and also has the support of one of two major political factions in the Kremlin, led by Deputy Prime Minister Igor Sechin. Ever since Rosneft assimilated the broken pieces of former Russian energy company Yukos (with help from a $6 billion loan from China in 2004), it has depended on developing its Siberian potential in order to rise above its many competitors. ESPO is therefore crucial to Rosneft’s survival and success. Therefore, Rosneft wanted to secure the deal with China first so as to have a stepping stone to a broader Far East strategy.

Negotiations on the Chinese deal were delayed. The Chinese were reluctant to sign an agreement while they had doubts about whether the Russian oil producer and pipeline builder could get along — specifically, China was waiting to see whether Rosneft would have the Kremlin’s support. Beijing also knew it had control of the purse strings; and given its inherent distrust of the Russians, it wanted to be sure that the agreement was fully to its liking — for instance, by insisting, against Putin’s demands, that the loan be made in U.S. dollars and not Russian rubles. China also wanted to make sure it did not need the cash to address any immediate problems at home due to the financial crisis.

Ultimately, the Kremlin intervened in the spat between Rosneft and Transneft, approving of Rosneft’s strategy and enabling the deal to move forward — by endorsing a slew of tax reforms and incentives for oil development and export in key East Siberian sites such as Sakha, Irkutsk, Krasnoyarsk, and eventually Taymyr, Sakhalin, Lena-Tunguska and Lake Baikal. The Chinese then came forward with the $25 billion, with a 6 percent yearly interest rate (moved down from 7 percent), which means that Russia gets the cash up front while China receives about 2.2 billion barrels of oil.

The deal reveals several things about the way regional geopolitics are unfolding as the world economy contracts. Russia and its state firms are in need of a lifesaver now that the combination of low oil prices, the absence of outside credit, and domestic financial troubles has rapidly depleted their reserves. The Chinese loan will provide an infusion of cash at just the right time to stave off financial pressures, allowing the Russians to undertake otherwise unfeasible projects that will pay off when Chinese energy demand revives. Moscow will see its Far East strategy advance another rung up the ladder, while Sechin’s clan, having scored a major victory in winning Kremlin approval for the Chinese deal, will gain an economic and political advantage over rivals.

China, meanwhile, will receive a steady stream of oil for the next 20 years. Rosneft’s facilities are ready to produce about 313,000 bpd (slightly more than the agreed-upon amount to repay the loan) at Vankor, the key Siberian site for the ESPO project. This amount of oil to be paid to China is roughly the same as the amount imported from Russia in 2007 (mostly by rail), and about half as much as the 600,000 bpd rail capacity in the region. This is significant, especially for a country so dependent on manufacturing and sensitive to energy shocks. China needs a reliable energy supply and does not want to be overly dependent on energy from one source. Moreover, most of its oil is shipped via ocean from the Middle East, and this leaves China at the mercy of U.S. naval power. However remote the possibility of an interdiction, it is enough to make a landlocked oil supply route attractive to Beijing.

But for Russia the deal is not a win-win. Moscow is getting pounded by the recession, and the decision to go forward on a pipeline that goes directly to China, forgoing the possibilities offered by a more versatile sea port destination, is a major concession. Obviously, now the Russian firms have to go through with the infrastructure developments, which will be technically demanding and fraught with unforeseen expenses and delays (sending Siberian oil eastward is said to cost twice as much per barrel as sending it westward). And the Chinese got a steal: Although not all of the contract’s subtleties are likely out in the open right now, reimbursement for the loan means that the Chinese have purchased Rosneft crude for only about $11.40 a barrel once interest is figured in — about one-third of what Russia’s crude fetches on the open market right now. The Russians have essentially locked the fate of their Far East strategy to the whims of Chinese energy policy, and this is a compromise that could reveal how financially desperate Russia is.

--- eof

No comments:

Post a Comment